Disclaimer: Before you start, we need to tell you upfront we are not a licensed financial planning firm. We are simply an education company, who will give you factual information. We do not give any general or specific advice around options, trading, or anything else. That is not what this course does. Please see a licensed financial planner when it comes to any investment advice you need. The purpose of this article is to report on various strategies and techniques observed by other traders in the use of this particular strategy. It is not a recommendation and this information must be handled responsibly. Any personal preferences offered by the author are intended to demonstrate to the reader how they think in analysing options strategies. They are not a recommendation to trade or not to trade.

The arguments can get quite heated. Scoffing, groaning, exasperation, shaking of heads, and yet amongst it all I’ve also seen dignity – those not getting caught up in the debates but quietly achieving the results in their own accounts. When traders get together and compare strategies, things can get quite colourful. And one of the issues they can get quite heated about is the safety of a naked put. What’s all the fuss about? Why are they so contentious? It all comes down to the issues of risk and safety.

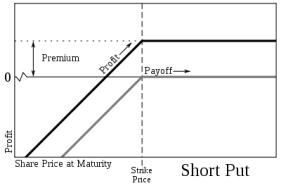

WHAT IS A NAKED PUT?

A naked put trade is when a trader will sell the right for a buyer to PUT their stock to them at a particular strike point. As there is no underlying stock in the account if the contract is exercised or goes into-the-money the trade is known as “naked”. It is exposed and is viewed as a liability.

Just as there is a metaphor around the traps for covered calls known as “share renting”, so naked put trading has been referred to as “selling insurance.” The trader is selling “insurance” every month on a particular stock hopefully with risk measurements in place to “insure” people’s stock positions, while picking up their premiums for cash flow.

Let’s look at an example.

Brian notices XYZ shares are trading at $10. He believes that the stock will rise but decides that if he had to own it he would happy to pay $9 for it. So he writes 3 naked put option contracts at $9 for the month. The option is $0.40 so he receives an upfront payment of:

$0.40 x 100 x 3 = $120

Margin required for the position is $1,200.

Return on investment (ROI) = 10%

The broker holds margin for the position to allow for fluctuations in the market in case it goes against Brian to cover the liability. The margin requirement will fluctuate dependant on whether the trade goes Brian’s way, i.e. whether the position remains out of the money, and time value. Provided the position stays out-the-money the time value will decay and so will the brokers requirements on that much margin.

The broker holds margin for the position to allow for fluctuations in the market in case it goes against Brian to cover the liability. The margin requirement will fluctuate dependant on whether the trade goes Brian’s way, i.e. whether the position remains out of the money, and time value. Provided the position stays out-the-money the time value will decay and so will the brokers requirements on that much margin.

The liability is that if XYZ stock is $9 or less Brian must take on the stock at $9 regardless of what the market value of XYZ stock is at the time of expiry. So if XYZ stock is only worth $5, Brian must pay $9 for each share and contract.

So the maximum risk to Brian if XYZ stock went to $0 in value is:

$9 x 100 (unit of shares per contract) x 3 contracts = $2,700

The probability of the stock ending at $0 at expiry may be low but you can see how he is running a metaphorical insurance company.

Now let’s look at how a naked put strategy may play out in the various markets:

Naked put in a bull market

The stock goes up to $11.

Brian keeps his $120 profit

Naked put in a flat market

XYZ stock is trading at $10.

Brian writes a 3 contract put at $9 for XYZ receiving $0.40 per contract premium

Profit = $120

The stock goes down to $9.90

Brian keeps his $120

Naked put in a bear market

XYZ stock is trading at $10.

Brian writes a 3 contract put at $9 for XYZ receiving $0.40 per contract premium

Profit = $120

The stock goes down to $8.

Brian’s is now either liable for 3 contracts of XYZ (300 shares) worth $8 and must cover the $1 gap at $9 strike.

Let’s look at the consumer market around insurance for a moment. Do you insure your house or car? And do you make a claim every year on those policies? It is highly improbable that people who hold house or car insurance make a claim every year. And yet even if we don’t claim, the vast majority in the Western world will still buy insurance and renew their policies even if they don’t use it. Why? Most of us buy insurance to have “peace of mind”. It covers us for the “just in case” “what if” uncertainties of life. Whether it is home and contents insurance, car, life, total and permanent disability, we are basically saying if the worse happens I want to know that my wealth, and the well-being of my family is secure.

With the exception of people shorting the market this is why traders buy puts. They are protecting a trade position of stock over a period of time, just in case the market turns and takes a dive.

Now let’s look at it from the insurance company’s perspective. Statistically they know that most people will not claim on their insurance every year. They also know how to place the odds in their favour so that their insurance policies are not just limited to one area. In the case of protecting housing from storms their policies and market area is not limited to one town or city. It is spread. They also have studied the statistics on natural disasters in that area, and assessed the risk to insure.

For example will an insurance company charge more if there is more risk? Absolutely! This is why the premium for new drivers under 25 is higher than those over 25. Generally over 25’s have been driving for some time. Statistically they have concluded there’s a higher risk in insuring the less than 25 age group and charge accordingly. So what they are doing is managing their risk and charging accordingly.

An insurance company also accepts they will have losses during the year. There will be customers who claim and will act on their policies. Provided they are selling more un-claimed policies than claimed then statistically they should be ahead.

And so it is with the naked put seller. However, the crunch comes when the market does go against them. Their success rate is determined by how good their ‘protection policies’ are then.

At the time of this writing I don’t trade naked puts or covered calls for that matter. But in my trading development my focus did shift from covered calls to naked puts as a better strategy. I don’t necessarily hold that view now. After this experience I discovered more sophisticated methodologies to trade and refined my thinking, but I’d like to give you an insight on how I arrived at these conclusions.

I started preferring a naked put over a covered call. One of the reasons for this was leverage. I discovered I could get more leverage trading a naked put option as opposed to a covered call. This allowed more funds for other trades, not having funds tied up in holding the stock.

Secondly, what appealed to me was the concept of “flying under the radar”. I rationalised that if the stock price fell I could fly under the radar provided there was some buffer between the stock price and the sold strike price, without having to worry about stock price fluctuations affecting the capital. However, if I owned the stock the fall in price would have a direct loss in the capital I required to buy the stock. So for example for a stock trading at $7.20 I could sell a put at $5. If the stock rose I would be in a successful trade, if it went flat I had a successful trade, and if it fell slightly but not at my strike point I was in a successful trade.

Secondly, what appealed to me was the concept of “flying under the radar”. I rationalised that if the stock price fell I could fly under the radar provided there was some buffer between the stock price and the sold strike price, without having to worry about stock price fluctuations affecting the capital. However, if I owned the stock the fall in price would have a direct loss in the capital I required to buy the stock. So for example for a stock trading at $7.20 I could sell a put at $5. If the stock rose I would be in a successful trade, if it went flat I had a successful trade, and if it fell slightly but not at my strike point I was in a successful trade.

Additionally, I liked the idea of acquiring stock at what I considered to be wholesale rates rather than retail rates. What do I mean by this? Well if I wanted to own the stock anyway, rather than pay the market value of what it was trading at as you would with a covered call minus the call sale, I rationalised I could get the market to pay me to take it off them at “sale price”. What I struggled with until my first mentor came, was how to systemise it. But when we did meet I needed no convincing on his methods. I had arrived at similar conclusions in my thinking.

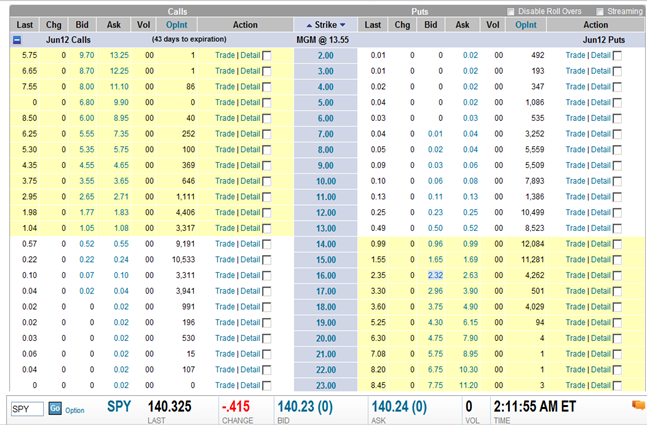

My mentor then mentioned that premiums on puts were generally higher than calls and looking at the options chain below there are more out-of-the-money put contracts trading than out-of-the-money call options.

However, the difficulty I found was what if the market did go against you in a naked put it could really sting! And the challenge was trying to discover what you could do to get rid of the liability.

Many people have attributed the saying to Warren Buffet “It’s Only When the Tide Goes Out That We Learn … Who‘s Been Swimming Naked”. Whether he actually said that or not is debatable.

What my second mentor taught me in his observations as a hedge fund trader was, “Naked put traders may get away with it for a while but when the market really swings against them, they get wiped out!”

You can see the debate emerging already! The great danger is when a trader doesn’t leave enough capital to cover the contracts they have written. When the market crashes they have to buy back the contracts they’ve written at much higher rates. The intrinsic value has increased. If there are few defence mechanisms they can get stung.

My personal trading experience when using this strategy was that when the market did go against me I gave all my profits back and started over again.

Having said this in my consultancy role I have heard of traders using it to trade successfully especially if they want to own that stock in the first place, and have traded in such a way to allow enough capital to do so. So what occurs is they sell the contract and receive the upfront premium. They may be exercised with the stock at the end of the month. If this occurs some opt to then trade a covered call over it to receive a premium to release it. If it goes against them some sell the stock immediately or determine at what point they will do so and follow it religiously.

I’ve also heard of sophisticated traders using this method targeting undervalued stocks in their fundamental analysis. So they have systems in place to define this, target it and then engage a naked put strategy to acquire it.

HOW DO YOU EXECUTE A ROLL OR MORPH?

If a naked put ends up in-the-money there are various decisions a trader must make.

Before expiry, depending on their strategy, they need to decide if they should buy to close (BTC) or be exercised and acquire the stock. There are extra brokerage costs either way but on a large account this is negligible.

If they decide to acquire the stock and be exercised they have the option to hold onto the stock and see if it will meet support and return to its previous levels. If they do this they then will need to decide if they hang onto to the stock, sell it or convert it into a covered call.

If they decide to buy to close (BTC) they need to recognise that the in-the-money options will have increased since they sold the option if it was previously out-of–the money. Additionally, these option premiums increase in the final two weeks before expiry. The market makers realise many are trading beyond their capital to acquire the stock, and so they make the traders pay more in the premium price gap than if they were exercised at expiry.

This is what my naked put options mentor would do. If he was in-the-money and wanted to roll down to a safer strike point he would Buy to Close (BTC) the in-the-money put option, sell to open (STO) another contract for the same size for the current month at the new at-the-money strike point, AND then sell to open (STO) a further contract of the same contract size or slightly more, for the following month. This sounded very scary to many traders as he was doubling the exposure on potentially a diving stock. He was a professional horse gambler from way back and knew the mathematical game of odds which he played. He had a knack for trading and wasn’t afraid to be exercised which many avoided.

In many situations when he could sense a stock was in a bearish trend he would simply stay out of the trade or lessen his trading in the market as a whole.

WHAT ARE THE PROS AND CONS OF A NAKED PUT?

Pros

The pros for naked puts are they are generally profitable in a bull and flat market.

They offer more leverage in that capital is not taken up by owning stock for the trade. Because they don’t own stock they are less affected by smaller price fluctuations in the underlying stock. I personally liked them as they could fly under the radar. Because there was more leverage there was greater return on investment and the premiums tend to be higher for puts than calls.

For those who want to own the stock, this method may be a profitable way to do so at wholesale rates, and they are paid upfront for the trade.

Cons

The downside for a naked put is you can’t trade them in a Self Managed Super Fund (SMSF) as they generally use margin. However, creative accountants do know ways around this.

When the market goes very bearish a naked put trader can pay a large price to close the positions and incur losses. In some situations they may be significant, especially if margin is used and risk is not managed.

Naked put trading will always come down to how risk adverse a trader is.

What I always admired about my mentor was while many disagreed with his methods he was getting results that worked for him. While he defended his strategy and explained it to me, he never entered those debates the other traders threw at him. He didn’t need to. His trading results were his story.

REFERENCE

Picture: Wikipedia