Disclaimer: Before you start, we need to tell you upfront we are not a licensed financial planning firm. We are simply an education company, who will give you factual information. We do not give any general or specific advice around options, trading, or anything else. That is not what this course does. Please see a licensed financial planner when it comes to any investment advice you need. The purpose of this article is to report on various strategies and techniques observed by other traders in the use of this particular strategy. It is not a recommendation and this information must be handled responsibly. Any personal preferences offered by the author are intended to demonstrate to the reader how they think in analysing options strategies. They are not a recommendation to trade or not to trade.

Trading is a funny game. I often said, “We all know what the upside may be, it’s the downside that you have to consider.” It’s always a game of risk vs reward.

Trading is a funny game. I often said, “We all know what the upside may be, it’s the downside that you have to consider.” It’s always a game of risk vs reward.

So far in our strategies we’ve gone from one extreme to the next in the sense that we have looked at what is regarded in the industry as a more conservative strategy of the covered call. All the bases of the liability with the underlying asset are covered in a covered call. With a naked put none of the underlying asset is covered. Now with spreads the pendulum swings to somewhere in the middle.

For traders who are more risk adverse than a naked put trader, but who want more liquidity than a covered call trader, spreads may satisfy the need for protection and offer a bit more flexibility.

WHAT ARE SPREADS?

A spread covers a wide range of variations when it comes to the various option strategies. Let’s look again at that extensive list which we observed at the start of this course …

- 1. Covered calls

- 2. Naked puts

- 3. Reverse Spread Ratios

- 4. Straddles

- 5. Strangles

- 6. Condors

- 7. Butterflies

- 8. Option Spreads

- 9. Bull Put Spread

- 10. Bear Call Spread

- 11. Ratio Spreads

- 12. Calendar Spreads

- 13. Time Diagonal Spread

- 14. Long Straddle

- 15. Short Straddle

- 16. Long Strangle

- 17. Short Strangle

- 18. Reversals

- 19. Conversions

- 20. Index Options

Naturally many refer to “spreads” in their names. However, others use various forms and combinations of spreads such as butterflies and iron condors. It can be argued they are forms of spreads with more layers to them. So a basic understanding of spreads is important. They will apply to other different trades in various forms.

What a spread does is contain at least 2 legs or components in the trade. There’s a sold component and a bought component at 2 different strike points over the same derivative.

Generally, in this style of trading the concept is the cash flow is made in the sale of the option rather than buying. Some options trades do buy, and try to increase the value of the trade with the intrinsic value. Personally, I prefer to make my money up-front in the sale, and for simplicity, we’ll focus on this style in learning the next stage.

Secondly, there is the bought component which is traded for protection. If the trade goes against them they want to limit their loss.

Let’s look at two examples – bull put spreads and bear call spreads.

They both refer to the direction the market may go.

So a bull put spread is suggesting the market is bullish and that a put spread is the way to profit as the market trends upwards.

A bear call spread is the opposite. It suggests the market is bearish and that a call spread is the way to profit as the market trends down.

You can see how a trader can now potentially make profit in the 3 market directions of up, down or sideways provided they pick the right direction and apply the right strategy.

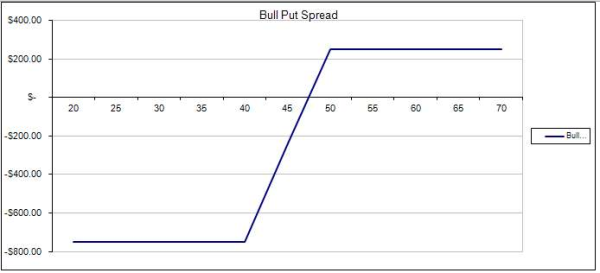

Let’s walk through a bull put spread.

A bull put spread is where the trader simultaneously sells puts at or out-of-money, and in the same transaction buys puts further out-of-the money at a further strike price than the sold leg, with the same contract size in both transactions.

So let’s see how this plays out …

Brian decides that ABC stock is bullish and he thinks that puts will be profitable as the market pulls upwards. ABC is currently trading at $20.

So Brian’s guidelines allow him to place a trade with a 10% buffer from the current market price.

So he decides to sell 8 contracts at $18 and buy 8 contracts at $17. There is a $1 strike gap between his sold and bought leg. What this is saying is that he is willing to lose a dollar if the market plummets. To get into the trade let’s assume he will receive $0.70 for the puts premium he sells at $18. He will pay $0.45 for the puts premium at $17.

So the profit he may gain from placing this trade is calculated as follows:

Sold puts – bought puts

Sold puts = $0.70 x 100 x 8 = $560

Bought puts = $0.45 x 100 x 8 = $360

Total profit = $560 – $360 = $200 (excluding brokerage)

We are going to use the abbreviations below more frequently.

- Sell to open (STO)

- Buy to close (BTC)

- Buy to open (BTO)

- Sell to close (STC)

To summarise Brian’s positions we would say he has:

ABC is $20

STO 8 X $18 PUTS

BTO 8 x $17 PUTS

PROFIT = $200

So how does this trade work in the various markets?

Bull market on a bull put spread

Stock goes up to $22 at expiry.

Brian keeps his $200 profit.

Flat market on a bull put spread

Stock goes to $20.20 at expiry.

Brian keeps his $200 profit.

Bear market on a bull put spread

Stock goes to $16 close to expiry. Hopefully Brian has taken action before things have got this bad, but let’s look at it anyway.

ABC is $16

STO 8 X $18 PUTS

BTO 8 x $17 PUTS

The liability is the concern here as he is obligated to come up with the stock at $18. However he has also bought protection to draw the stock to himself at $17 over the same contract size. Therefore, Brian’s loss is $1 x 100 units x 8 contracts = $800 as opposed to $2 x 100 units x 8 contracts = $1,600. PLUS we have to remember he made money upfront when he entered the trade of $200. Therefore, total loss is $600. His loss is limited in this instance.

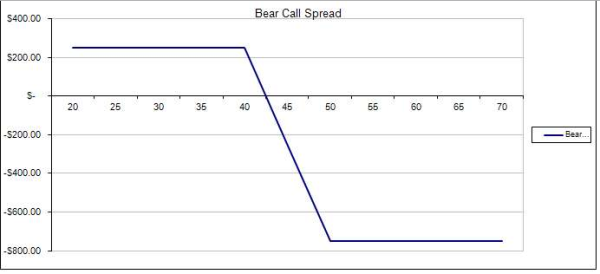

Let’s look at bear call spreads. They are simply the opposite of a bull put spread.

A bear call spread is where the trader simultaneously sells calls at or out-of-money, and in the same transaction buys calls further out-of-the money at a further strike price than the sold leg with the same contract size in both legs.

So let’s see how this plays out …

Brian decides that ABC stock is bearish (going down) and he thinks that calls will be profitable as the market goes down. ABC is currently trading at $20.

So Brian’s guidelines allow him to place a trade with a 10% buffer from the current market price.

So he decides to sell 8 contracts at $22 and buy 8 contracts at $23. There is a $1 strike gap between his sold and bought leg. What this is saying is that he is willing to lose a dollar if the market trends upwards and puts his trades in-the-money. Let’s again assume he will receive $0.70 for the call premium he sells at $22. He will pay $0.45 for the call premium at $24.

So the profit he may gain from placing this trade is calculated as follows:

Sold calls – bought calls

Sold calls = $0.70 x 100 x 8 = $560

Bought calls = $0.45 x 100 x 8 = $360

Total profit = $560 – $360 = $200 (excluding brokerage)

To summarise Brian’s positions we would say he has:

ABC is $20

STO 8 X $22 CALLS

BTO 8 x $23 CALLS

PROFIT = $200

So how does it work in the various markets?

Bear market on a bear call spread

Stock drops to $18 at expiry.

Brian keeps his $200 profit.

Flat market on a bear call spread

Stock goes to $20.20 at expiry.

Brian keeps his $200 profit.

Bull market on a bear call spread

Stock goes to $24 close to expiry. Again, we hope Brian has taken action before things have got this bad but let’s look at it.

ABC is $24

STO 8 X $22 CALLS

BTO 8 x $23 CALLS

The liability is the concern here as he is obligated to come up with the stock at $24. However, he has also bought protection to draw the stock to himself at $23 over the same contract size. Therefore, Brian’s loss is only $1 x 100 units x 8 contracts = $800 as opposed to $2 x 100 units x 8 contracts = $1,600 PLUS his upfront profit of $200 when he entered the trade. Total loss is $600.

His loss is limited in this instance.

You can see how the market can be traded either direction.

What if Brain was more on his toes when the trade was going against him?

What if Brain was more on his toes when the trade was going against him?

Let’s say the trade ended up between his sold leg and bought leg in both the bull put spread and bear call spread.

So the liability is now in-the-money, but the bought protection leg is out-of-the-money.

In the case of the calls let’s say that the stock ended up at $22.50.

ABC = $22.50

STO 8 X $22 CALLS

BTO 8 x $23 CALLS

If the stock stays here Brian will be in trouble if he doesn’t have enough in his account to come up with the stock at $22.50 ($22.50 x 100 units x 8 contracts = $18,000). If he calls the stock to himself at the $23 strike he would incur further loss with the market only trading at $22.50 not $23. He would need to perform a morph or roll of some sort.

HOW DO YOU EXECUTE A ROLL OR MORPH?

The closer Brian stays in this position as he moves towards expiry the harder it will be for Brian in terms of what his options are.

Let’s say it is several weeks before expiry. He may want to sit and wait to see if the stock will cool off and his sold position may move out-the-money once again. However, if it continues to stay in-the-money Brian must take action at some point. Determining when to do this is the difficulty. As for myself, I don’t like to have, sold in-the-money options in the last 2 weeks before expiry. The premiums to close out are higher than they should be.

Brain has the option to buy to close (BTC) the $22 calls and sell his bought options at $23.

The value of the $22 options will be higher than he sold them for as they are now in-the-money. However, his bought options will also be more valuable as they are now at-the-money as compared to being out-of-the-money when he first purchased them.

So he could simply sell his bought leg at $23 which helps mitigate the loss he has incurred by buying back his $22 position.

The longer he leaves this though the greater the likelihood that his bought options will be suffering from time decay and he will not receive the premium he would a number of weeks out before expiry.

The longer he leaves this though the greater the likelihood that his bought options will be suffering from time decay and he will not receive the premium he would a number of weeks out before expiry.

He can therefore either “wait and see” if things improve. Or he could close out the position. If he wants to defend his account size further he could choose to open up another trade that is in a safer position. i.e. Sell another spread further out-of-the money either for the current month or the following month depending on what the premiums have to offer on the options.

I go into greater details on this and especially how they apply in my favourite trade Reverse Spread Ratios in 12 Month Premium Classroom – Advanced Options Trading Course 201 that Trading Institute conducts. Additionally, in this course I show how I sometimes I apply the strategy theory of strangles and straddles to a reverse spread ratio which is even more advanced.

The application of a morph or roll over for a bull put spread is simply the reverse. The trader would wind up the trade and go for safer positions in lower out-the-money put options and may need to explore whether the trade for the current month or the following one should be pursued, subject to premiums on offer and how far the options are from expiry.

WHAT ARE THE PROS AND CONS OF SPREADS?

There are many variations on these basic spreads. And there are various pros and cons to them.

Pros

Spreads allow for greater protection if the trade goes against you.

The broker requires less margin to hold these trades as compared to trading them as naked trades. This is because they are covered at some level.

They give you leverage in that your account is not taken up in stock.

Cons

They get a little more complicated in the morphing or roll down sequences. So the skill level required is slightly higher.

They are less profitable than if you are trading naked as you have to spend sometimes up to 50% of your upfront premium on protection on the bought leg. So the return on investment is less.

Sometimes to enter a spread you actually have to have a $2 or $3 strike spread to make it profitable going into the trade. This means there is less protection if the trader is required to morph when defending.

Spread trades are more complex to fill when entering them into the market as compared to a simple naked put trade. In the case of spreads two legs must be filled. If a trader is entering a trade on a limit order they may have to be a bit more patient. More components have to line up and be accepted by the market.

The trader can also expect to be charged more brokerage to enter spread trades as there are more legs that are being dealt with. On smaller account sizes this may have an effect on profitability when you calculate brokerage fees. Similarly there may be further fees if a morph is required so there needs to be enough profit upfront for the exercise to work.

Spreads while a little more complex to trade especially if you have to morph or roll down certainly have many benefits. This must be weighed up by the trader to see if spreads suit them.

They are the basis for many other forms and variations of options so a basic understanding is important.

References

Picture references

http://optionstradingiq.com/wp-content/uploads/2011/01/Bull-Put-Spread.jpg

http://www.optionstradingiq.com/option-strategies/bear-call-credit-spread/

{kind=link}